Recent reports about the failure of sales at auction to achieve near reserve prices have been disputed by real estate market leader Ray White Real estate. Realty Media’s Kevin Turner talks to Ray White Managing Director Dan White. Read the full report below:

Ray White head disputes claim

Recent claims that property auction reserves are not being met around the country has come in for strong criticism from the leading auction group in the country – Ray White. Looking at auction data over the past months in regards to volume, auctions that do and don’t proceed, the highest offer prior, reserve price, final bids, and sale price gives the Ray White Group an interesting insight into auction performance and more broadly market performance. Ray White Managing Director Dan White says the ‘facts tell the real story’

The data focuses on the major cities of Australia.

Volume

As restrictions started to ease and we started to head in the colder months we have seen a pleasing and surprising lift in volume which considering the uncertainty in late March and April is very welcomed. In May across Australian major cities volume was down 37% compared to May 2019, in June 2020 the group was down 12% and what is great to see is that in July 2020 we are already up 27% on last year. From here the agent and vendor either push to auction day 64% make auction day, 14% sell prior or 22% are changed to private treaty, withdrawn or delayed.

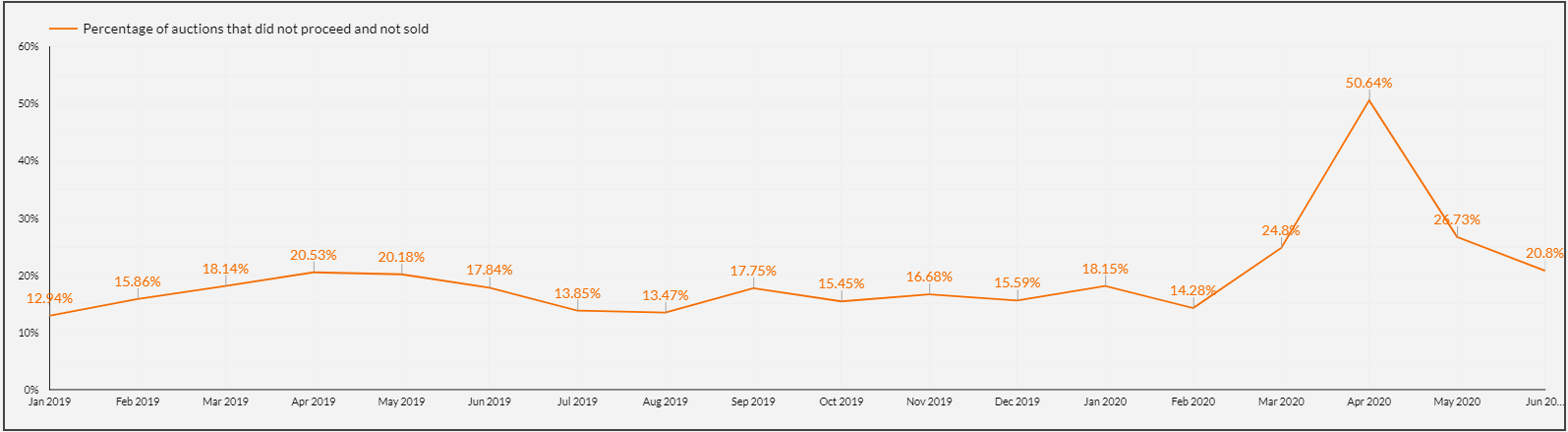

Auctions that do not make auction day

Scheduled auctions not making auction day are broken down into those that sell prior and those that are changed to Private Treaty, delayed or withdrawn completely from the market.

Auctions scheduled selling prior between Feb 2020 to April 2020 were the highest on record with on average 19% of RWG auctions scheduled selling prior. May and June dropped slightly sitting at around 15% of scheduled auctions selling prior. The long term average for the RWG is 14% of auctions selling prior.

Auctions that don’t make auction day excluding sold priors, not surprisingly dramatically increased to hit 50.6% of scheduled auctions not proceeding. The majority of these auctions were changed to Private Treaty. May and June dropped to approx 23% and based on the most recent week should continue to fall to be in line with the long term average for auctions not proceeding (excl sold) at 21.8%.

Auctions that proceed to auction day

Auctions that Pass In

The Ray White Groups’ long term average for auctions not meeting reserve sits at 13.5% below the reserve. Across the group, we haven’t seen any significant shift in auction offers/final bids as can be seen in the chart below showing the difference between reserve and highest offers/bids and the reserve price. On auction day the Passed In ratio sits at an even share between auctions that pass in on the highest bid and vendor bid approx 40% each and auctions where no bids are received at 20%. In fact, auctions that have active bidding hit an all-time high in Feb 2020 with 88% of auctions having bidding activity with May and June 2020 not far off with 85% of auctions having bidding activity. March and April 2020 were lower with some weeks having 30% of auctions having no active bidding.

Auctions that Sell on Auction Day

The group average for auctions that sell on auction day are being rewarded, selling on average 3.26% over reserve and 9.7% over the highest offer prior to auction. Again when looking at the most recent months the RWG has not had any significant shifts and currently the average sale over reserve sits at 1.5% and the highest offer prior to auction sits at 9% since April.

The gap between those auctions that don’t sell because the reserve is not met and those that do sell over reserve is a key metric that the group is focused on. Considering the recent and current commentary around the market, the rich and complete data collected from the network shows that where we sit now is not that different to where we were pre COVID.

Certainly, April and May had some challenges, June saw the group transition back to relative stability and July is showing positive signs. There are areas of focus around registered and active bidding that have been identified as areas that have come off the boil in the last 3 weeks, although from a very high base, but still areas to be monitored.